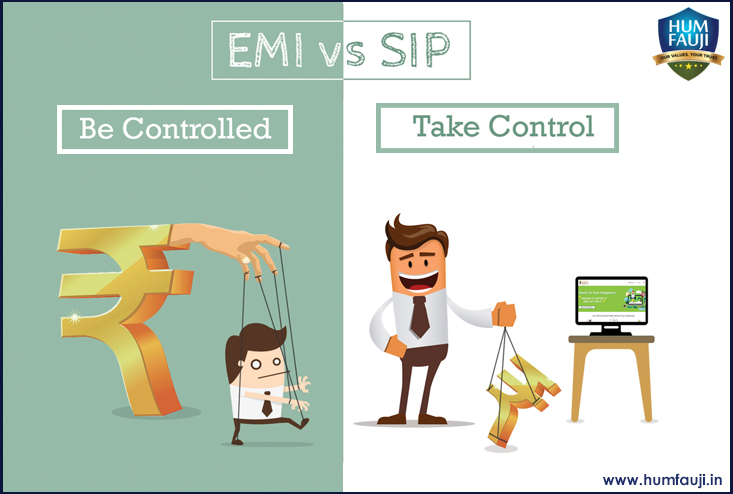

Invest in SIPs and take control of your Finances

Albert Einstein is supposed to have remarked: *Compounding is the 8th wonder of the...

Albert Einstein is supposed to have remarked: *Compounding is the 8th wonder of the...

Divesh Kumar has recently retired as a contended man. He hasfulfilled his duties as...