22Jun

Should You Exit Equity Now? The Costly Mistake Many Investors Make in Bad Markets

Should You Exit Equity Now? Or Stay Invested? Over the last few ...

06Jun

Should You Worry About Rising Interest Rates?

"The purpose of debt investments is not to win when interest rates move in....

30May

Why Has Everyone Suddenly Fallen in Love with US Markets?

Dear Investors, Jai Hind Over the last few months, one question has l...

31Mar

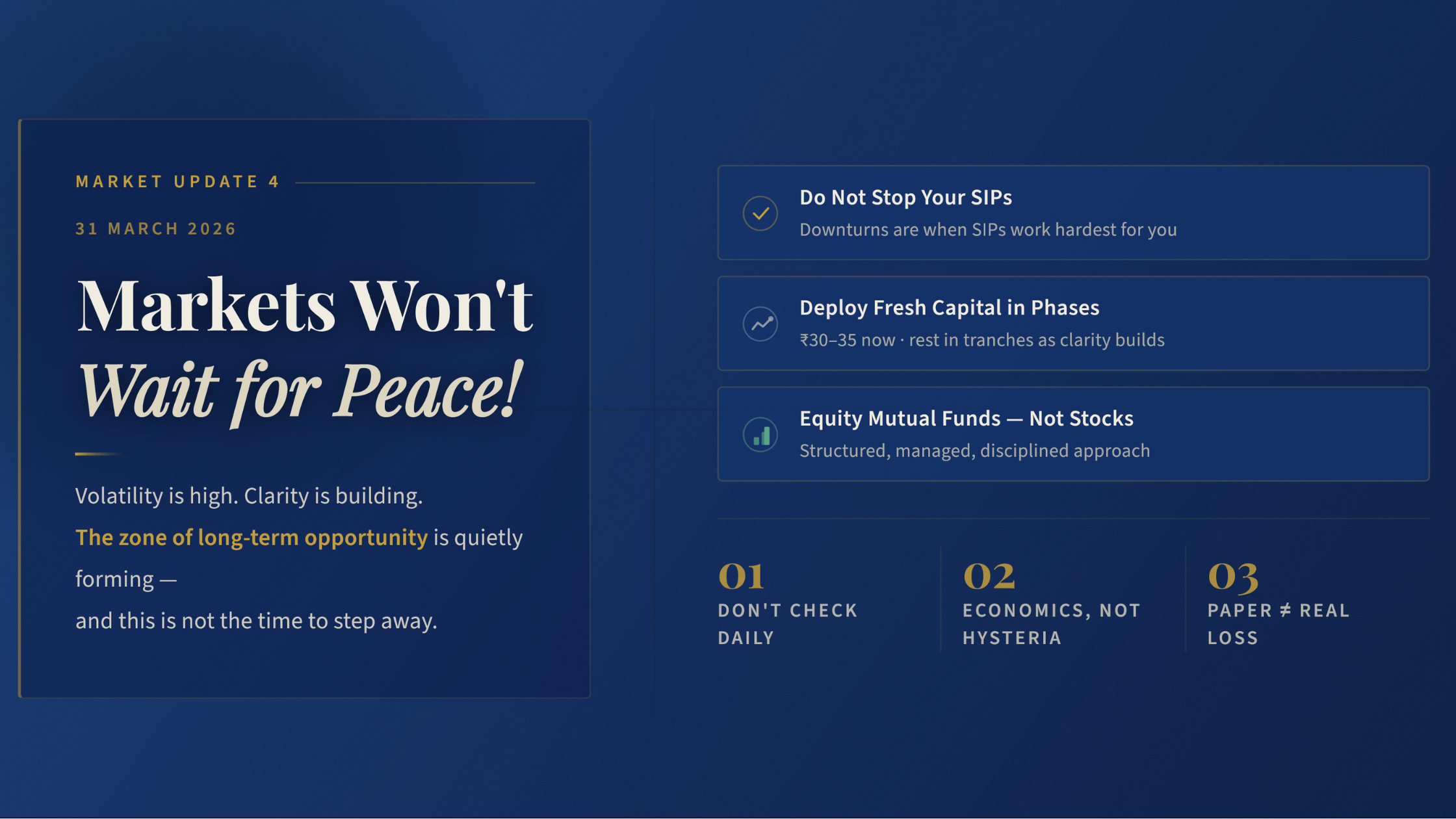

Market Update 4 : Markets Won’t Wait for Peace!

Markets Don’t Wait for Peace — And Neither Should You Investor Note | Ma...

23Mar

Market Update 3 : The Real Risk Today Is Not the War!

Markets, War & Investor Behaviour: What Really Matters Right Now Wee...

13Mar

Market Update 2 : Navigating Markets Amid Continuing Iran–US Conflict

What Should Investors Do During Geopolitical Conflicts? Weekly Investor ...

07Mar

Market Update: Staying Focused during Geopolitical Volatility

How Geopolitical Tensions Impact Markets — And What Investors Should Do ...

27Feb

Home Loan for Armed Forces Personnel: What Banks Don’t Tell You

For most families, buying a home is the biggest financial decision of their...

02Feb

Union Budget 2026–27: What It Means for You as a Retail Investor

The Union Budget 2026–27 continues the government’s focus on long-term stab...

28Jan

NRI Investments in 2026: Five Essentials to Stay on Course in a Changing World

Imagine this for a moment. You’re standing on the deck of a ship. The se...

16Jan