From Insurance to Retirement: All Your Money Matters —Under One Roof!

Did you know? Over 70% of Indians don’t have a proper financial plan. Even worse, more than 60% of their hard-earned money often lies idle in low-interest bank accounts. Not because they don’t want to invest—but because financial decisions are rarely simple.

Insurance is handled by an agent. Investments are advised by someone else. Tax-saving tips come from a third person. And retirement? That’s often left for “later.”

With so many pieces scattered, people either delay decisions or end up with half-baked plans that don’t really serve their future. For armed forces families, where stability and long-term planning are especially important, this lack of clarity can be a major hurdle.

That’s why there’s a growing need for a single, dependable solution—someone who understands your financial picture as a whole, not in parts.

This is where Hum Fauji Initiatives (HFI) steps in, we believe your financial well-being deserves more than scattered advice. You need one reliable place that understands your unique needs—especially if you’re from the armed forces community—and walks with you through every stage of life. Whether it’s ensuring your family’s safety through optimal insurance coverage, growing your wealth through strategic investment management, or planning for a secure retirement, we’ve got it all covered—under one roof and our approach is grounded in integrity, transparency, and expertise.

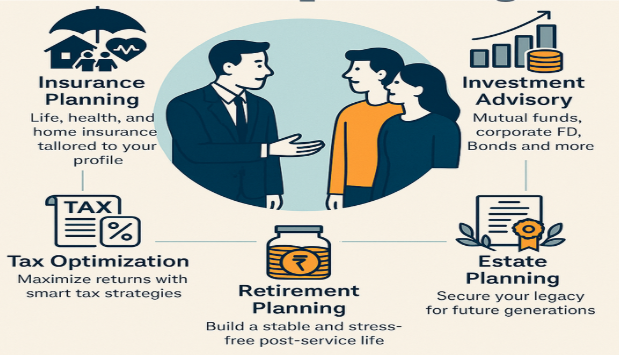

Our services include:

- Insurance Planning: Life, health, home—covered smartly and at lowest costs.

- Investment Advisory: Mutual funds, bonds, FDs, Gold and much more tailored to your goals, dreams and needs.

- Tax Optimization: Save the right way, without last-minute panic, the smart way.

- Retirement Planning: Build a stress-free life after service for yourself and your children.

- Estate Planning: Secure your family’s future, your way. Ensure your wealth passes to your rightful owners seamlessly when you’re not around.

Most importantly, we don’t sell products—we create a life-time financial plan with the right investment avenues based on your goals.

So, if you’ve ever delayed financial decisions because it felt “too much,” HFI is the simple, trusted partner you’ve been waiting for.

Let’s plan your future—clearly, calmly, confidently.

(Contributed by Mausam Gupta, Relationship Manager, Team Prithvi, Hum Fauji Initiatives)

How Compound Interest Can Help Your Child’s Savings Grow

As parents, we plan for everything—school admissions, extra-curriculars, even birthday themes. But how often do we plan financially for our child’s future?

Here’s a fact: Less than 35% of Indian parents actively invest for their child’s long-term needs. Most rely on ad hoc savings or fixed deposits or the latest financial advertisement that barely beat inflation. But if there’s one thing that can quietly work magic for your child’s future, it’s compound interest.

Compound interest means your money earns not just on the amount you invest—but also on the interest it already earned. Over time, this snowballs into substantial growth.

Remember how your DSOP is growing or has grown over time?

Let’s break it down:

- Investing ₹10,000/month from birth at 10% return could grow to ₹57 lakhs by age 18.

- But start the same investment at age 10, and it’ll barely reach ₹14 lakhs by age 18.

That’s the power of starting early. You don’t need big money—just discipline and time.

🔑 Three keys to grow your child’s savings smartly:

- Start a Children’s SIP as early as possible

- Stay consistent—even small monthly investments matter

- Use goal-based mutual funds instead of low-interest savings

There’s no “perfect” time to begin. But the earlier you start, the bigger the head start you give your child.

Time is the best teacher—and the best investor.

(Contributed by Riya Bhandari, Relationship Manager, Team Arjun, Hum Fauji Initiatives)

Breaking the Myth: Why Timing the Market is Impossible

It sounds like a perfect strategy—buy when the market dips, sell when it peaks, and walk away with great returns. But in reality, even top investors struggle to do this consistently.

Here’s why market timing doesn’t work:

🔹 Unpredictable Market Movements

Stock markets respond to countless factors—economic news, global tensions, policy changes, even emotions. Accurately predicting all of that? Nearly impossible. Nobody’s ever been able to it with any amount of consistency.

🔹 Missing the Best Days

Data shows that missing just 10 of the best days in a decade can halve (Yes, that’s 50%!) your returns. And often, the best days come right after the worst. Step out at the wrong time, and you may lose out big.

🔹 Emotional Decisions Lead to Mistakes

Fear in a falling market and excitement in a rising one push many investors to sell low and buy high—the exact opposite of what they should be doing.

🔹 Time in the Market Wins

History proves it: Staying invested consistently beats trying to jump in and out. Compounding only works if your money stays in.

So, Market timing may seem like a smart move, but it often leads to missed opportunities and unnecessary stress. A long-term, consistent investment strategy is the true key to wealth creation.

(Contributed by Anjali Singh, Relationship Manager, Team Arjun, Hum Fauji Initiatives)

What did our clients ask us in the last 7 days

Question – I’ve been thinking about using my mutual funds to pay off my home loan. I know my investments are doing well, but having a loan still bothers me. Could you please help me understand in what situations it makes sense to repay a home loan by redeeming a well-performing investment portfolio?

Our Reply –

It’s a common dilemma: your investments are growing well, but that lingering home loan still feels like a burden. So, should you redeem your mutual funds to repay it?

Let’s look at both sides of the decision—logical and emotional:

Financial Perspective:

- Interest Rate Vs Investment Return – If your mutual fund returns are higher than your home loan interest rate, staying invested usually builds more long-term wealth.

- Tax Benefits

Under the old tax regime, you can claim:

- ₹1.5L deduction under Section 80C (principal repayment)

- ₹2L under Section 24(b) (interest paid)

In the new tax regime, most of these benefits are there if it’s a let-out property.

Emotional Perspective

- Peace of Mind – Even if the numbers work, carrying debt can feel stressful. For some, debt causes emotional discomfort, even if it’s “good debt” like a home loan. Paying it off earlier offers you peace of mind, emotional relief, and a sense of financial freedom.

- Lifestyle and Life Stage Factors – If you’re nearing retirement, have variable income, or face big life events (job change, child’s education), reducing liabilities might offer more comfort and stability.

Situations When It Makes Sense to Redeem and Prepay:

- You’re in the new tax regime with no significant tax benefits from the loan.

- Your risk appetite has reduced, and you’re uncomfortable with market volatility.

- You’re close to a major life event (e.g., job change, retirement, child’s education) and want to reduce liabilities.

- You value emotional peace more than market returns

(Contributed by Team Arjun, Hum Fauji Initiatives)

📞 Still unsure? Speak with a Hum Fauji Initiatives advisor to explore what’s best for your financial journey.

Click here to reserve your slot now! Share this message with mothers in armed forces and mothers of armed forces officers in your network! We are eager to chat and Happy to Help 🙂