Investing: A Life-Skill Your Kids Can Learn Early!

Imagine giving your child a superpower—the ability to grow money!

Teaching kids about investing early helps them build a secure future, and the best part, learning about money can be fun at every age!

🧐For Little Learners (Ages 5-8): Money is Magic!

The “3 Jars Challenge” – Give them three jars: Spend, Save, and Share. This teaches the basics of money management.

Role-Playing Games – Let them play “shopkeeper” to understand transactions in a fun way.

Piggy Bank Growth – Show them how coins add up over time, just like a tiny plant growing into a tree!

🧐For Curious Tweens (Ages 9-12): Let’s Talk Money Smarts!

Stock Market = Shopping Mall – Explain how buying stocks is like owning a piece of their favorite brands.

Mini Investment Game – Give them pretend money to “invest” in brands they love and track performance.

Goal-Based Saving – Encourage them to save for something big to teach planning and patience.

🧐For Teens (Ages 13-18): Be the Boss of Your Money!

Risk vs. Reward Game – Teach them about safe (FDs), medium-risk (Mutual Funds), and high-risk (Stocks) investments.

Magic of Compounding – Show them how investing early multiplies money faster.

Track a Real SIP Investment – Open a small SIP in their name and let them track its growth!

Invest in Your Child’s Future Today!

Investing just ₹20,000 per month for 15 years at 12% returns could grow to ₹1.05 crore!

By getting them involved in tracking their investments, you’re giving them the tools to be financially savvy from an early age. The earlier you start, the more they’ll learn and grow. Start today—help your child build a future filled with financial freedom!

(Contributed by Yogesh Gola, Relationship Manager, Advisory Desk, Hum Fauji Initiatives)

Investment Myths: Separating Fact from Fiction in Finance

Investing is like navigating a jungle—you need a clear path, or you might fall into traps set by myths!

Let’s bust a few common misconceptions that could be holding you back.

Myth: Saving 20-30% of your income is enough for retirement if you or your family member will not get a Govt mandated pension

💡Fact: If things were this easy, retirement planning would not be the kind of challenge that it is. It is about replacing your post-retirement lifestyle costs, not just saving a fixed percentage. Given rising aspirations and inflation, a well-thought out action plan would be better than assuming that 20-30% savings rate is sufficient. A well-structured financial plan is essential to building an adequate retirement corpus.

Myth: High returns can make up for low savings

💡 Fact: Chasing high returns is like hoping to win a jackpot—it’s not a strategy but playing Blackjack in a casino! A sudden market crash could leave you stranded.

The best approach? Save more and stay consistent.

Myth: SWPs (Systematic Withdrawal Plans) from hybrid funds are the perfect retirement income source

💡 Fact: Hybrid funds carry market risk especially if they have higher equity component. Withdrawing during a downturn could shrink your savings. A balanced mix of stable, liquid investments to draw SWP from is the key for stress-free retirement income.

Don’t let myths guide your money—separate fact from fiction and invest wisely!

(Contributed by Neeraj Kumar, Relationship Manager, HNI Desk, Hum Fauji Initiatives)

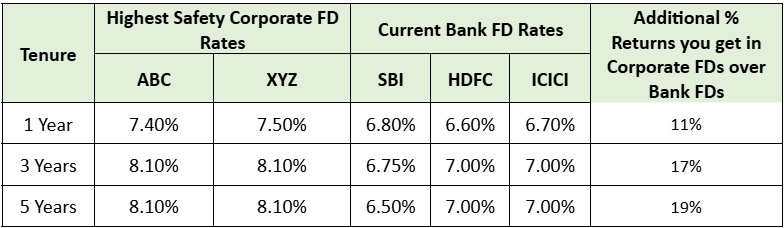

Safe Investments That Pay: An Overview of Corporate Fixed Deposits

If you’re looking for a safe yet rewarding way to grow your savings, Corporate Fixed Deposits (FDs) might be just what you need! Offering higher interest rates than traditional bank FDs, they strike a balance between growth and security.

But are they right for you? Let’s break it down.

Why Choose Corporate FDs?

Higher Returns – Corporate FDs typically offer better interest rates than bank FDs, helping your money grow faster.

Security & Stability – Investing in companies with strong credit ratings ensures peace of mind with fixed returns.

Flexibility – You can choose your investment tenure and how often you receive interest—monthly, quarterly, or annually.

Corporate Vs Bank FDs Interest Rates Comparison

💡 Very high safety Corporate FDs also consistently offer much higher returns across different tenures, making them an attractive option for investors seeking better yields.

Things to Keep in Mind

- Check the company’s credit rating to ensure reliability.

- Diversify your larger investments to balance risk and reward.

Corporate FDs can be a smart way to earn more on your savings without taking excessive risks.

(Contributed by Bhawana Bhandari, Financial Planner, HNI Desk, Hum Fauji Initiatives)

What did our clients ask us in the last 7 days

Question – Whenever I invest in mutual funds, I notice that instead of the full amount being allocated, the units allocated are of slightly less amount. Why does this happen?

Our Reply –

This happens due to the Govt stamp duty, which is charged at 0.005% of the investment amount. Introduced in July 2020, this charge applies to all mutual fund investments—equity, debt, and ETFs—whether in physical or demat mode, including SIPs, STPs, and dividend reinvestments.

Some investors assume that there is some kind of entry load being charged on investments. It is not so. Entry load was abolished from Mutual Funds more than 15 years ago in 2009.

It’s important to note that this stamp duty does not affect redemptions or switches out to other funds.

Should You Worry?

- This small cost is part of the regulatory framework and doesn’t significantly affect your overall returns being very tiny, 0.005%.

- Staying informed helps you make smart financial decisions.

- Focus on long-term investment goals rather than such small charges.

By keeping your focus on the bigger picture, you can navigate such fees without letting them disrupt your financial strategy.

(Contributed by team Prithvi, Hum Fauji Initiatives)

Wish to discuss more about it? Schedule a Call Here.