Love, Laughter, and Lakhs: Managing Wedding Budget

Indian weddings are serious affairs. They resemble a Bollywood extravaganza, complete with lavish dinners, dancing events, and an abundance of drama and there’s a price to all of this fun, usually a high one.

But do not worry, we’re here to guide you through the financial maze that is an Indian Wedding.

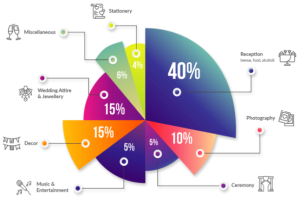

Face the Facts: First things first, let’s talk numbers. According to a recent survey, the average Indian wedding costs a whopping Rs 25 lakhs! That’s enough to buy a small apartment or fund a world tour. The ‘big, fat Indian Wedding’ can of course run into so many crores that a number of zeros may be difficult to count…

Now, take a deep breath and remember: it’s just an average. Your wedding can be anything you want it to be, from a budget-friendly affair to a full-blown Maharaja-style extravaganza.

Negotiate Like a Pro: Remember, bargaining is an art form in India. Don’t be afraid to haggle with vendors. From decorators to caterers, everyone ‘expects’ a bit of negotiation.

Embrace the Off-Season: Who says monsoon weddings can’t be magical? How about a winter wonderland wedding? Opting for an off-season wedding can save you big bucks on venues, decorations, and even travel costs for out-of-town guests.

Embrace the Digital World: E-invites are eco-friendly and budget-friendly. They’re also easier to track and manage than traditional paper invites. Plus, you can have fun with the design and add interactive elements like links to locations, posts, videos, etc.

Be aware of hidden costs: On your wedding day, unexpected expenses can completely throw you off. Very often, a wedding programme exceeds the scheduled time fixed with the venue. Inquire about the overtime rules before hiring the venue.

Remember, your wedding should be a celebration of your love, not a financial burden to be carried for a long time after it is over. With a little planning and creativity, you can have a beautiful and memorable wedding without breaking the bank.

So, go forth, lovebirds, and plan your dream wedding!

(Contributed by Aman Goyal, Relationship Manager, Team Vikrant, Hum Fauji Initiatives)

Financial Check-Up: Mark these Check Points before the year ends

As the curtain falls on 2023 and the stage is set for the grand welcome of 2024, let’s take a moment to indulge in a bit of financial nostalgia. Our pockets may be lighter from festive expenditures, but fear not! It is a good time to reflect on your financial journey.

Check Point 1: Review your budgeting journal

Budgeting is key to managing your finances. Following the 50/30/20 budgeting method, allocate 50% to needs, 30% to wants, and 20% to savings and investments. This balance allows you to enjoy the present while securing the future.

Benjamin Franklin famously said, “Beware of little expenses – a small leak can sink a great ship.”

Check Point 2: Building Emergency Fund

Emergency funds are the superhero cape your portfolio needs. When you’re in financial trouble, 3-4 months’ worth of expenses in the piggy bank (aka your emergency fund) can battle the unexpected financial villains.

Check Point 3: Insurance Planning

Ensure all family breadwinners have a life insurance shield, And don’t forget to get adequate health insurance for your family’s well-being. Keep your assets, like homes and cars, protected with insurance too!

Check Point 4: Tracking Financial Goal.

Whether it’s your child’s education, retirement, or buying a house, calculate the required investment and start investing or mapping existing investments, preferably through a systematic investment plan (SIP).

Pro Tip: Add the flavor of top-up SIPs to your investments for the timely achievement of your financial goals.

Bonus Check Point: Succession Planning

As you twirl through investment portfolios, ensure your assets are left in capable hands with a Will. If you’ve got one, dust it off and make sure it’s ready to include any new investments from the year.

As the year bows out, assess your financial performance and swap out the unnecessary ones and the underperformers. Set the stage for the New Year, the brand new 2024, with a roadmap of milestones for a smooth financial journey.

(Contributed by Hemant Bisht, Associate Financial Planner, Team Vikrant, Hum Fauji Initiatives)

What Did Our Clients Ask Us in the Past 7 Days?

Question – How can my son manage his mutual fund investments in India while working abroad as an NRI for the next five to seven years?

Answer – It is a common misconception that Non-resident Indians (NRIs) are not allowed to invest in India. The reality is that they can easily invest just by following guidelines set by the Reserve Bank of India (RBI) and the Securities and Exchange Board of India (SEBI) under the Foreign Exchange Management Act (FEMA). Here are some important things to be aware of about your Indian investments and your finances in general when you become an NRI:-

1) Update your Residency Status in KYC Records.

2) Convert your Bank Account to NRE or NRO, as per your fund inflows and outflows.

3) Don’t forget additional Compliances such as FATCA declaration form for US or Canada Residents.

4) Tax implications on NRIs’ fund investments in India be well known to the investor.

5) India has a Double Taxation Avoidance Agreement (DTAA) with over 90 countries. You need to be clear of the tax implications of your Indian investment in both, India and your country of residence.

Please note, actively managing NRI investments requires planning, strategic choosing of accounts and investments, and regular monitoring. Consider seeking professional guidance for portfolio management and to ensure your son’s financial goals are met even while abroad.