23Mar

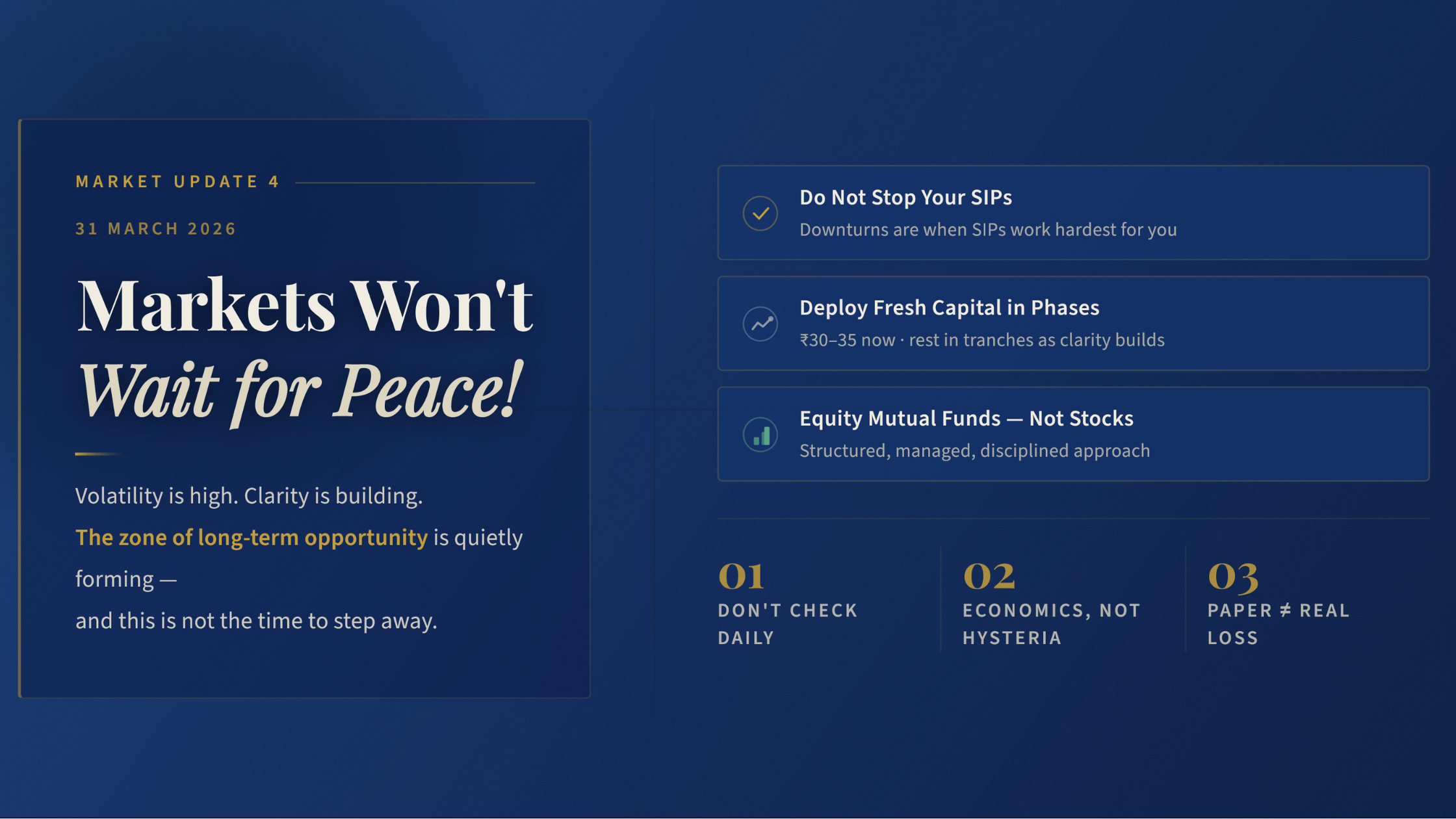

Market Update 3 : The Real Risk Today Is Not the War!

Markets, War & Investor Behaviour: What Really Matters Right Now Wee...

17Nov

Loan Against Mutual Funds for Indian Armed Forces Personnel

A perfect overdraft facility that is accessible quickly and comes without d...

07Nov

Secure Your Family’s Future with the Best Insurance Advice for Armed Forces

Life in the armed forces is a journey of honour, courage, and sacrifice. Wh...

01Nov

Best Term Insurance Plans for Armed Forces Officers and Veterans

During active service, the armed forces officers are mandatorily covered un...

26Sep

Health Insurance for Armed Forces Officers—Serving, Retired and their families

Serving in the armed forces is a matter of pride. Gratefully, the...

28Aug

Why Armed Forces Personnel Need to Have Adequate Life Insurance?

While life insurance is a protection that everyone with dependants must hav...

28Aug

Premature redemption price of gold bond fixed at Rs 5,115 per unit

Mumbai: The price for premature redemption of sovereign gold bond (SGB) due...

31Jul

Secure Your Future: Corporate Fixed Deposits for Veterans and Armed Forces Officers

Like many defence veterans, you want to protect what you’ve earned over the...

04May

Still Relying on Bank FDs? Discover a Smarter, Safer Alternative!

Are your savings really growing in your bank FD — or just sitting idle whil...

01Nov

The Safe Investment Option for Armed Forces Officers and Veterans

When it comes to investing, trust and safety are top priorities — especiall...

14Aug