17Nov

Loan Against Mutual Funds for Indian Armed Forces Personnel

A perfect overdraft facility that is accessible quickly and comes without d...

07Nov

Secure Your Family’s Future with the Best Insurance Advice for Armed Forces

Life in the armed forces is a journey of honour, courage, and sacrifice. Wh...

01Nov

Best Term Insurance Plans for Armed Forces Officers and Veterans

During active service, the armed forces officers are mandatorily covered un...

26Sep

Health Insurance for Armed Forces Officers—Serving, Retired and their families

Serving in the armed forces is a matter of pride. Gratefully, the...

18Sep

Best Home Loans for Fauji Families: A Specialised Service Handpicking the appropriate Home Loan for Armed Forces Families

Hum Fauji Initiatives walks beside our Armed Forces families not ...

28Aug

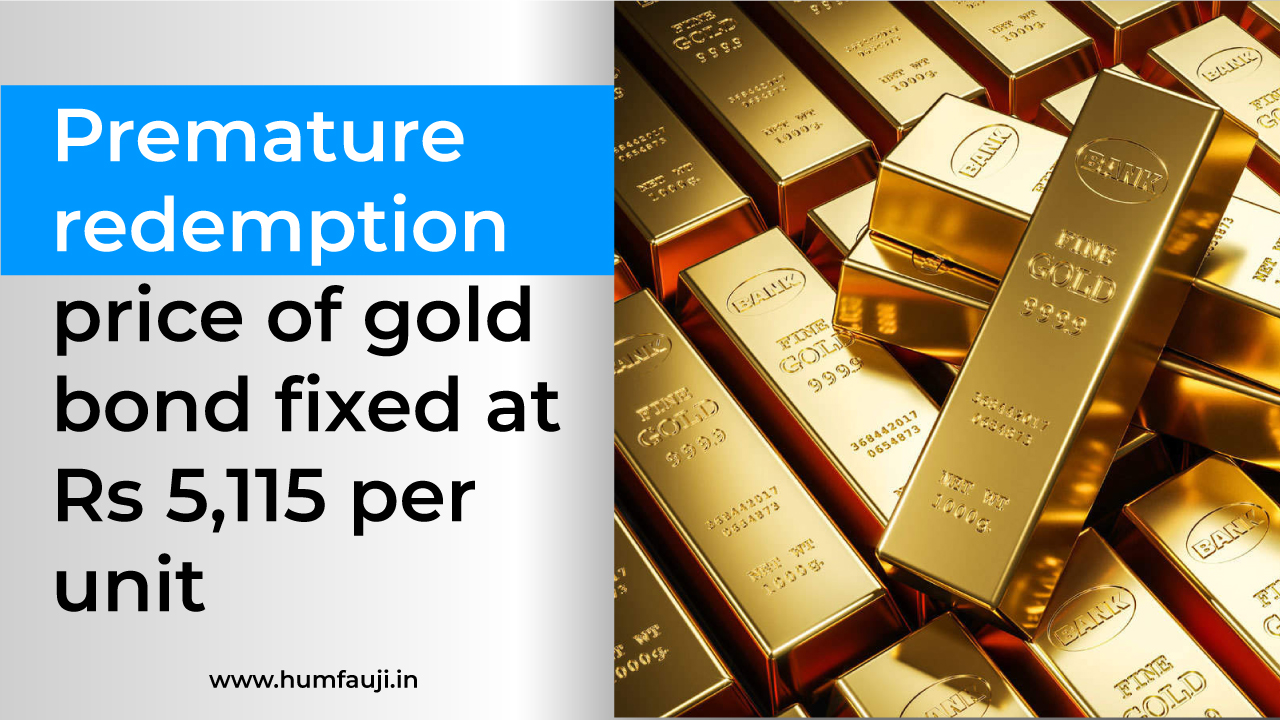

Premature redemption price of gold bond fixed at Rs 5,115 per unit

Mumbai: The price for premature redemption of sovereign gold bond (SGB) due...

28Aug

Why Armed Forces Personnel Need to Have Adequate Life Insurance?

While life insurance is a protection that everyone with dependants must hav...

21Aug

The NRI’s Guide to Investing in ETFs: Building a Borderless Portfolio in Indian & Global ETFs

Whether you are an NRI by choice, an OCI in the UK, or an......

31Jul

Secure Your Future: Corporate Fixed Deposits for Veterans and Armed Forces Officers

Like many defence veterans, you want to protect what you’ve earned over the...

29Jun

Your 2025 Tax Filing Starts Here! Smarter, Faster, Simpler

(for Financial Year (FY) 2024-25 corresponding to Assessment Year (AY) 2025...

04May