Dear Friends,

I had written a series of two articles some time back comparing Commutation of pension Vs Non-Commutation, and recommended that everybody should commute pension due to the reasons outlined there. Now, for the officers who have retired on or after 1st Jan 2016, the Govt has given an option to further commute the additional basic pension accruing due to the 7th CPC (Central Pay Commission) recommendations. In this article, I will deal with this dilemma whether the officers who have retired on or after 1st Jan 2016 should opt for further commuting their additional basic pension or not.

Rather than writing a lot of words, I have taken the indicative data of four officers of the ranks of Lt Gen, Maj Gen, Brig and Col, all of whom have superannuated on 1st Aug 2016 at their respective ages of 60, 58, 56 and 54 years of age and compared the effect of additional commutation Vs non-additional commutation. To keep the things simple, I have assumed that all of them have commuted 50% of their pensions earlier. Similalry, while calculating their tax liabilites, I have assumed that they will take full advantage of the Rs 1.5 Lakh exemption limit of IT Sec 80C. In case of officers having tax-free pension due to Diability or Gallantry Awards, the only small difference will be the tax part.

Details of Commutation and Pension as per 6th CPC

The Table 1 below gives out how the four officers of different ranks retiring on the same day and commuting 50% pension would be receiving their pension and would have received the commutation amount. If they have invested their commuted amount prudently, avoiding (or at least not committing much amount to) ‘apparently’ safe investments like bank FDs, PO MIS, Senior Citizen Savings Scheme (SCSS), Insurance etc, they would be patting their backs on their decision to commute their pension – whether goaded by my earlier articles on commutation or their own personal decision to do so.

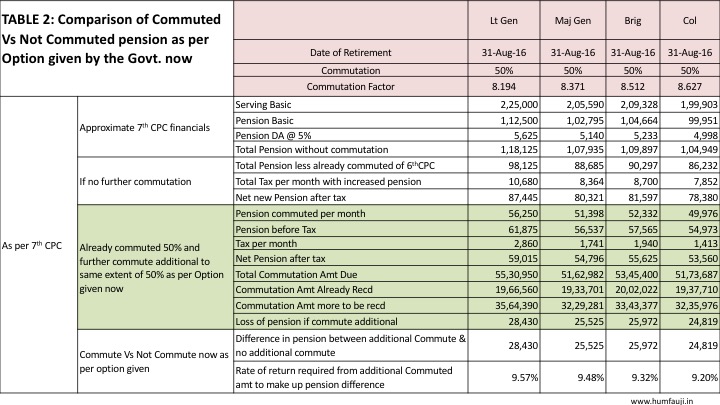

Comparison Commuted Vs Not Commuted pension as per Option given by the Govt now

Table 2 below gives out the financials as per 7th CPC for the four ranks now and paints two scenarios – if you do not commute your pension any further beyond what you’ve already done (ie, 50%) under 6th CPC; Or if you decide to avail the option and further commute 50% of the increased basic pension as per 7th CPC.

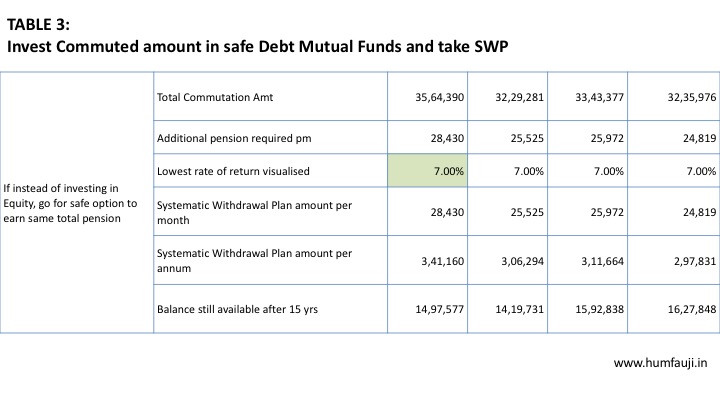

It can be noticed that the so-called shortfall amount can be easily made up if the amount received as additional commuted amount is invested in financial instruments which yield approximately 9.4% average per annum. On a long term basis, a mutual fund portfolio of 35% Equity & 65% Debt can achieve this average return. If an officer wants to be very safe and invest in a 100% safe Debt portfolio and one assumes a very comfortable 7% per annum returns from this portfolio of very high quality Debt Mutual Funds, the commuted amount received can be used to give out additional pension through the Systematic Withdrawal Plans (SWP) route. The advantage of using this mode would be:-

- The non-commuted pension is fully matched due to additional returns from the portfolio.

- Taxation would be much less for first three years of SWP pension compared to tax on uncommuted pension since SWP has a component of Principal which is never taxed. Hence, only a part of the pension is taxed compared to uncommuted pension being fully taxed.

- After three years, indexation benefits kick in into the investment portfolio and rate of interest goes down as per inflation. Most likely, there will be Nil tax after five years on the SWP pension for the next 10 years or so when the commutation is restored back.

- As the table below shows (Table 3), you will have a substantial amount of money balance after 15 years even while your pension is fully matched for the 15 years of commutation vis-a-vis no additional commutation option.

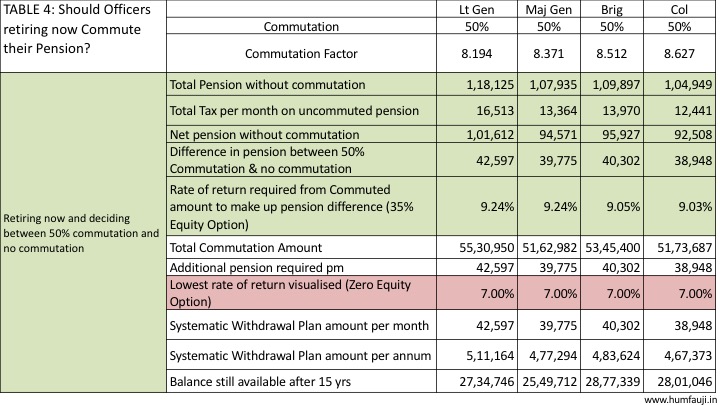

What should you do if you are retiring shortly?

What should you do if you are retiring shortly?

While the above cases dealt with the additional commutation option that the Govt has given to the officers who have already retired on or after 1st Jan 2016, what should the officers retiring hereafter do? I sincerely believe that if the officer invests his retirement corpus well, including the commuted amount, there is no reason why maximum commutation option of 50% should not be taken by each and everybody. The Table 4 below depicts the same. If you are prepared to invest the retirement corpus in about 35% equity, you do not have to touch your commuted corpus and can earn the same pension as uncommuted option WHILE STILL HAVING YOUR ENTIRE COMMUTED CORPUS INTACT. And if you do not wish to go in for any equity at all, a full debt option, yielding 7% returns only, will also leave you with a large amount of money 15 years later. Thus obviously, non-commutation is only going to make you poorer!

Summarising,

Why you should definitely commute your pension to the maximum extent allowed?

I summarise the benefits of commutation brought out in my two articles earlier below:-

- The pension is fully taxable while the commuted amount is fully tax-free. If this commuted amount is properly invested, just a fraction of the tax would need to be paid compared to the tax on uncommuted pension while getting the same net pension.

- With prudent investing without taking any or small risks with a small part of your commuted amount, you can have your same amount of pension vis-à-vis non-comutation while having a large amount with you throughout your life.

- There would be a large bulk amount available in hand which is a big asset to deal with emergencies, financial goals and responsibility or simply to lead a much better lifestyle.

- Since commutation is a one-time exercise, the commuted amount per month remains static. So while the pension rises continuously due to DA, pay commissions and now OROP, the commuted amount deduction is continuously reducing to be a smaller proportion of the pension. Eg, when I took my PMR in April 2010, my commuted amount was Rs 19,375 per month which was big proportion of my overall pension. Now it is a very small proportion of my Rs 77,000 net pension.

- If something untoward happens to you, your family will get the same pension since the Govt disregards the commuted amount paid, irrespective of whether you commuted or not. Clearly, non-commutation in such cases is a big financial loss to the family.

If you wish to read our last article on Commutation, it is available here.

For more information, feel free to reach us on, contactus@humfauji.in or call + 011 – 4240 2032, 40545977, 49036836 or

Subscribe to our blog for regular financial updates or follow us on Facebook | Twitter | Linkedin

Comments (6)

Sir,

I have sent a query on your email as mentioned above.

The question is, ‘When would we get the arrears of Gratuity and Commutation’? Our entire financial planning hinges on the total amount received and the time-line. As of now, those who have retired recently (by Sep 2017), cannot be sure on the actual arrears and the date of receipt, and are forced to hold on the present emoluments in the hope for substantial investments in a planned way.

I retired from the rank of col in AMC in Dec 2014. Will I be getting any arrears

No Sir, You will not be getting any arrears other than what you’ve already received.

Sir, I am going to retired as Havildar. my pension is Rs. 20438. what is the good option whether to commute or not.

If I receive full pension I will be getting Rs. 245256/annum, near to low tax slab Rs.250000.

If I commute 50% of my pension, I will get Rs. 10719 (whether my pension for next 15 yrs is Rs. 10719? )

My commuted amount is .Rs.1175146.( Commutation value-9.136).

For 15years if I didn’t get 50% of pension i.e. Rs.10719, it comes around Rs. 1929420. Then I will lose Rs.1929420-Rs. 1175146= Rs. 754274.

Please explain…whether it is good to commute or not?

Thank you

Commutation should be decided on the basis of whether you need a bulk amount or more monthly amount. Bulk amount requirement is linked to your future big expenses coming up while monthly requirement is linked to what are you going to do after retirement, how much will you earn and if it is sufficient for you on a monthly basis. Look at commutation more as a low-interest loan taken from the Govt which you pay over 15 years.

And whenever you take a loan, you pay an interest – obviously you will pay back more than you borrow. Commutation can be done of any percentage from 0 to 50%, and DA is never commuted. Hence you get DA on full pension even if you commute.